Published Oct 2025

Vietnam’s Automotive Industry Sees Surge in Imports and Diversification in 2025

Vietnam’s automotive industry saw a surge in CBU vehicle and auto parts imports in the first nine months of 2025, driven by rising consumer demand and expanding domestic manufacturing. Indonesia, Thailand, and China remained key suppliers, while local giants like VinFast and THACO led parts imports.

Vietnam’s automotive industry has witnessed robust growth in imports of completely built-up (CBU) vehicles and auto parts during the first nine months of 2025, signaling both rising consumer demand and industrial expansion in the domestic market. This growth reflects broader trends across Southeast Asia, as Vietnam continues consolidating its role as a key automotive manufacturing and assembly hub.

Strong Growth in CBU Automobile Imports

In the first nine months of 2025, Vietnam imported an estimated 155,321 CBU automobiles, valued at USD 3.406 billion, representing an increase of 24.2% in volume and 32.8% in value compared to the same period in 2024.

In August 2025 alone, the country imported 16,274 vehicles worth USD 363.3 million, up 8.5% in volume and 22.6% in value year-on-year. Although there was a slight month-on-month decline from July, the overall trend remains upward, indicating sustained demand throughout the year.

The growth is driven primarily by passenger cars and light trucks, with imports increasing steadily since the beginning of the year. Analysts expect this momentum to continue through Q4, supported by expanding credit availability, promotional campaigns, and the rise of middle-class purchasing power.

Key Import Markets: Indonesia, Thailand, and China Lead the Way

Indonesia remained the largest supplier of automobiles to Vietnam in the first eight months of 2025. Imports reached 51,955 units valued at USD 736.3 million, accounting for over 40% of the total CBU market.

Thailand ranked second with 47,334 units valued at USD 935.1 million, followed by China, which supplied 30,506 units worth USD 993.7 million.

- Imports from Indonesia and Thailand mainly consisted of passenger cars with up to 9 seats and pickup trucks.

- China, in contrast, exported mainly trucks and specialized vehicles, resulting in a higher average unit value.

Other active suppliers include Japan, Russia, Germany, South Korea, the United Kingdom, and the United States. Notably, German and Russian vehicle imports showed sharp growth, reflecting shifting supply chains and diversification efforts by Vietnamese importers.

Industry Dynamics: Rising Competition and Consumer Choice

The sharp rise in import volumes highlights both consumer demand recovery and increased market competition after several challenging years. While the average unit value of imported vehicles has declined, the broader product mix suggests that consumers now have more choices across price segments.

However, experts caution that this also raises challenges for manufacturers and distributors in maintaining quality standards and competitive pricing. The growing market complexity may force automakers to adjust pricing strategies, strengthen distribution networks, and invest in after-sales services.

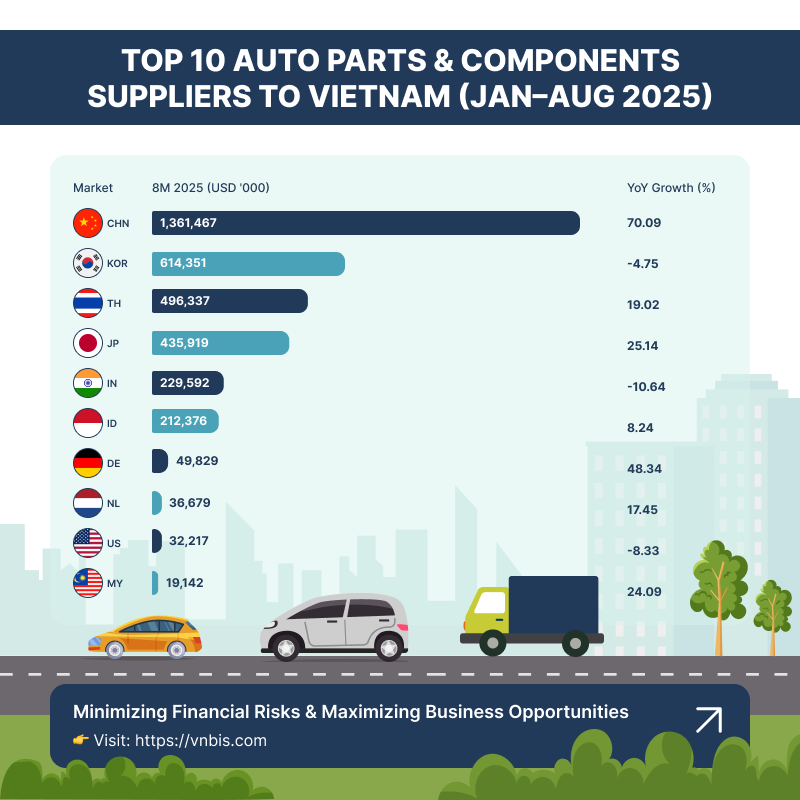

Auto Parts and Components Imports: Strong Growth and Market Concentration

Importing auto parts and components is critical in supporting Vietnam’s fast-growing assembly and manufacturing sector.

- In August 2025, auto parts and components imports reached USD 452.2 million, up 6.1% year-on-year.

- For the first eight months, total import value hit USD 3.614 billion, up 23.4% compared to the same period in 2024.

- By September, this figure was estimated at USD 4.114 billion, reflecting steady demand from domestic automakers.

China remains the dominant supplier, accounting for over 40% of total imports, with shipments surging 70.1% year-on-year. Other major suppliers include South Korea, Thailand, and Japan, representing over 80.5% of the total import value.

Some European suppliers — Germany, the Netherlands, and Spain — also recorded notable growth, suggesting increasing diversification of Vietnam’s sourcing structure.

Notable growth was recorded from Japan (+18.5% YoY in August), the Netherlands (+34.1%), and the Philippines (+40.4%), showing broader sourcing trends.

Major Importers: Domestic Manufacturers Drive Demand

The demand for imported components is primarily driven by domestic assemblers and manufacturers, many of whom are part of large joint ventures or foreign-invested enterprises.

Top importers in the first eight months of 2025 included:

- VinFast – USD 486.8 million

- Ford Vietnam – USD 297.2 million

- Hyundai Thanh Cong – USD 273.1 million

- THACO Group – multiple subsidiaries across Mazda, KIA, Premium, Bus, and Truck

- Toyota, Honda, Isuzu, and Mercedes-Benz

These companies account for a significant share of Vietnam’s total auto parts import value, underscoring their central role in domestic assembly and supply chains.

Export Activities and Regional Integration

While imports dominate, Vietnam is also increasing its participation in global and regional automotive supply chains:

- Domestic manufacturers are beginning to export auto parts and accessories to neighboring ASEAN markets, the EU, and North America.

- Vietnam benefits from free trade agreements such as the EVFTA, RCEP, and CPTPP, which help reduce tariffs and create favorable conditions for both imports and exports.

- A growing number of multinational suppliers (e.g., Bosch, Bridgestone, Michelin) have expanded their local production and supply base in Vietnam to serve both domestic and export markets.

This dual structure, importing high-value components while developing local production capacity, is gradually positioning Vietnam as a regional automotive production and assembly hub.

Outlook: Opportunities and Strategic Shifts Ahead

The automotive industry is expected to continue expanding in late 2025 and beyond, supported by:

- Strong consumer demand, especially for small and mid-sized vehicles;

- Policy incentives encouraging local assembly and localization of parts;

- Infrastructure upgrades and improved logistics;

- Vietnam’s strategic position in ASEAN supply chains.

However, the growing dependence on imported components, particularly from China and other Asian suppliers, poses challenges for domestic value-added production. Policymakers and businesses are under increasing pressure to:

- Localize supply chains,

- Invest in technology transfer,

- Support supporting industries, and

- Enhance export competitiveness.

Conclusion

The first nine months of 2025 have marked a dynamic phase for Vietnam’s automotive sector, with strong import growth, diversifying supply chains, and active domestic manufacturing participation.

As the country integrates with global markets, strategic investments in local production, R&D, and supply chain resilience will determine how well Vietnam can transition from a highly import-dependent market to a competitive automotive manufacturing base.